Investment banking interviews are demanding. To earn an offer, you must demonstrate a mastery of valuation methodologies and a deep intuition for the drivers behind them.

To help you prepare, below is a list of valuation questions asked at top investment banking firms. We identified these by analyzing 200+ Glassdoor interview reports specifically for analyst roles at Goldman Sachs, J.P. Morgan, and Morgan Stanley.

From that analysis, we’ve selected the 10 most common valuation questions and included tips, a prep plan, and sample answers to help you structure strong responses and feel confident going into your interviews.

- What to expect in IB valuation interviews

- Different types of IB valuation interview questions (with answers)

- More examples of IB valuation questions (by company)

- Tips for acing IB valuation interviews

- How to prepare for IB valuation interviews

Click here to practice 1-on-1 with investment banking ex-interviewers

Let’s get started.

1. Overview: Investment banking valuation interview questions

Before we go through the most common topics in investment banking valuation interviews, let’s first take a look at what these interviews are and how they work.

1.1 What are IB valuation interview questions?

As an investment banking analyst, you’ll spend a significant portion of your time building models to advise clients on acquisitions, divestitures, or capital raises. Valuation questions assess whether you have the technical foundation to carry out these core responsibilities.

You will be evaluated on your ability to determine a company’s worth using both financial models and market data. This requires more than just formulaic knowledge.

According to Hashim (Ex-Lazard Analyst, ex-J.P. Morgan), valuation questions go beyond a simple "Walk me through a DCF" problem. You’ll be tested on your technical intuition, or your ability to explain how a change in the financial statements ripples through to the final valuation.

Oftentimes, these questions are integrated with accounting principles to see how adjustments affect an asset's total value. For example, an interviewer might ask: “How does a $10 increase in depreciation specifically affect a Discounted Cash Flow (DCF) valuation?”

You must show you’re able to project a business's future performance and translate those expectations into a single value today. This involves justifying your assumptions, selecting the appropriate methodology for a specific industry, and articulating the relationship between risk and reward.

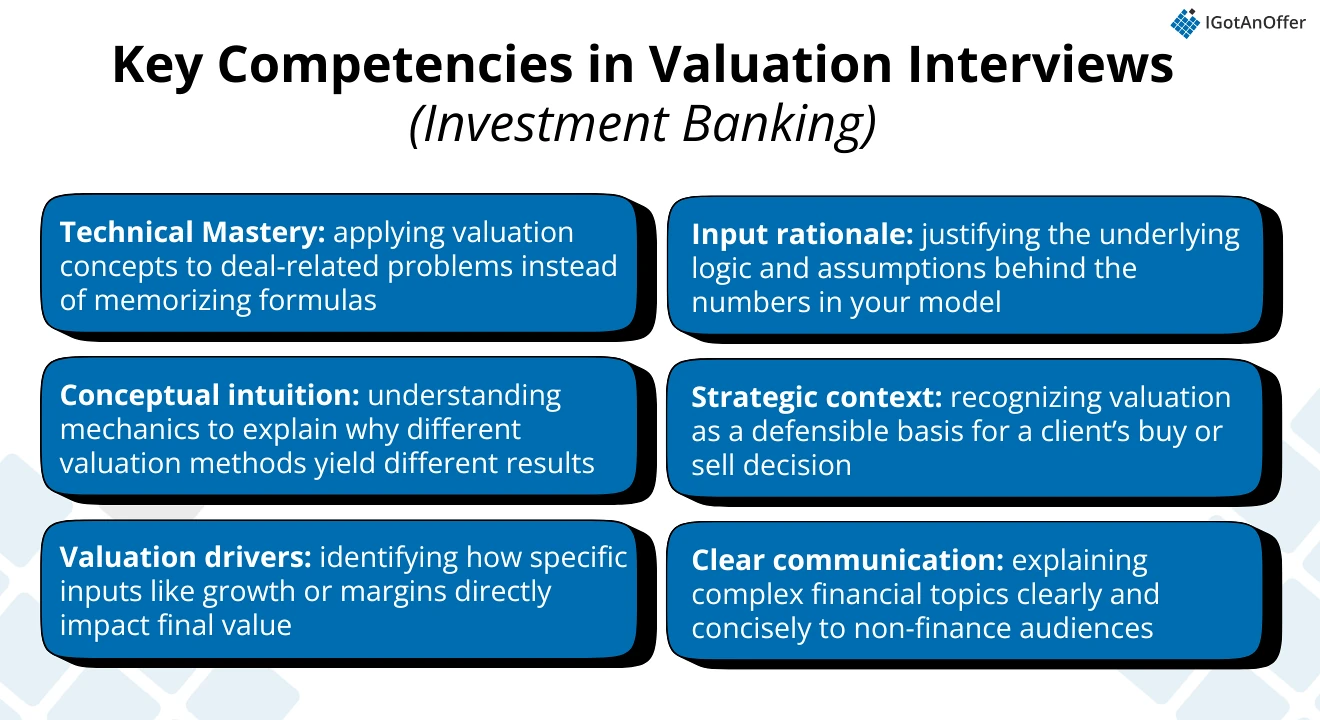

1.2 What competencies are being tested in IB valuation interviews?

According to investment banking experts Hashim (Analyst at Lazard, ex-J.P. Morgan), Susan (ex-Goldman Sachs IB Associate), and Wayne (Sr. Strategy Consultant at Kearney), you will be evaluated on the following criteria:

- Technical Mastery: As an IB analyst, you must be able to apply valuation concepts to specific, deal-related problems instead of memorizing scripts or formulas (e.g., can you explain Enterprise Value vs. Equity Value)

- Conceptual Intuition: You need to understand the mechanics well enough to explain why different methods yield different results (e.g., why a DCF might produce a higher value than a Trading Comps range, or why EV/EBITDA is more appropriate than P/E for a capital-intensive business)

- Valuation Drivers: You should be able to identify how specific inputs (e.g., revenue growth, margins, etc.) directly impact the final valuation of an asset.

- Input Rationale: Don't simply cite numbers. You must justify the underlying logic of your assumptions and explain how those inputs function within the context of the overall model.

- Strategic Context: IB analysts should be able to "think things through" by recognizing that the ultimate purpose of any valuation is to provide a defensible basis for a client to buy or sell an asset at an appropriate price.

- Communication Under Pressure: You are expected to explain these financial concepts concisely and clearly. A true indication of mastery is being able to explain complex topics simply enough for a non-finance person to understand.

1.3 IB valuation interview expectations per level

Technical expectations in valuation interviews vary by role, but the bar generally becomes higher with increasing seniority. According to coaches Susan, Wayne, and Jonathan, here’s how expectations typically differ by level.

Summer Analyst (Internship)

For summer analyst roles, technical questions will focus on your foundational knowledge and mental agility. Interviewers want to confirm that you understand the basic valuation methods and how they relate to one another.

You are not expected to build precise models, but you should be comfortable explaining the logic behind common valuation frameworks and performing quick mental math.

Full-Time Analyst (Entry-Level Hire)

For full-time analyst roles, technical interviews are more applied. Interviewers will often ask you to explain valuation assumptions, walk through impacts, or reason through how changes in the market affect an asset's price.

At this level, you must show a deeper understanding of valuation methodology, including which methods are most applicable to specific sectors and what typical metrics are used to evaluate companies in those industries.

Associate (MBA or Lateral Hire)

The associate level is where you can expect to get more questions around application and judgment. You may be asked how you would structure a valuation analysis, evaluate key assumptions, or challenge an analyst’s work. There would also be more mental math involved.

Because this is a more senior role, interviewers want to see that you can manage the rapport between senior VPs and junior analysts. You must demonstrate that you can provide clear guidance to your team and offer alternate viewpoints on valuation results.

Coaches who contributed to this guide

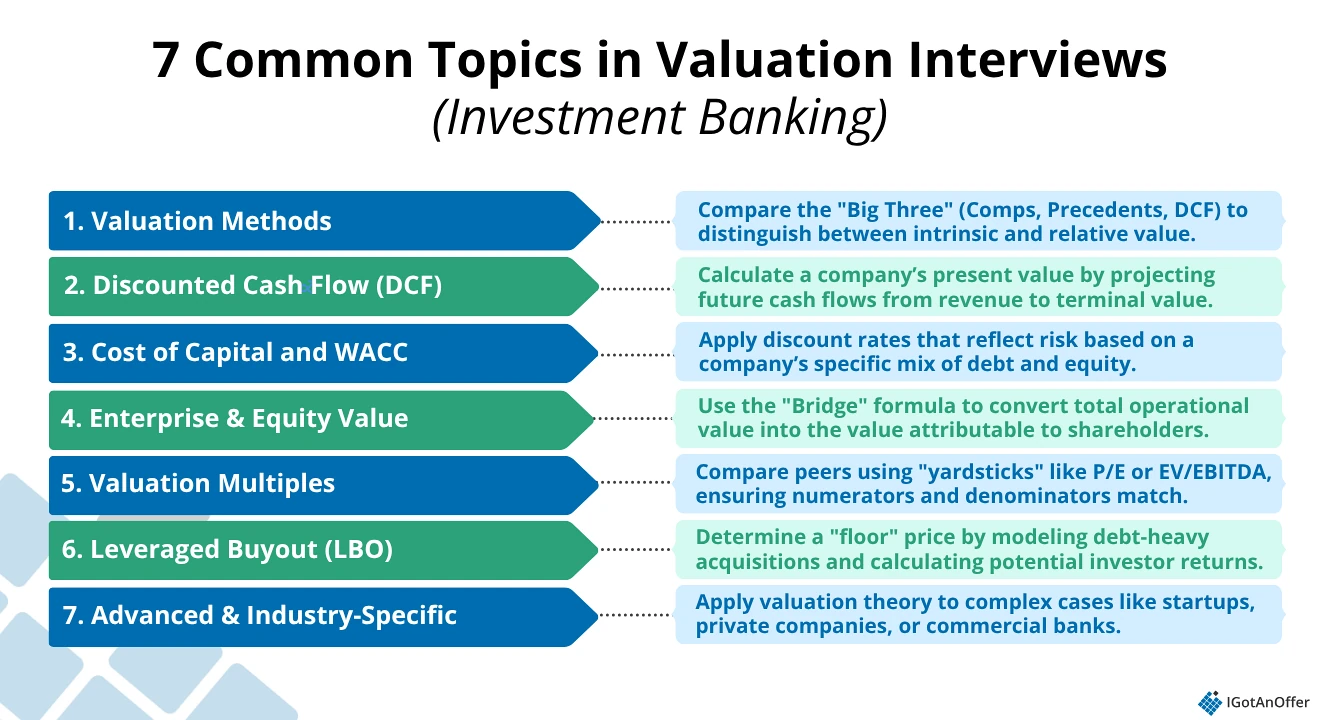

2. 7 different topics covered in IB valuation interviews (+sample questions, answers) ↑

The valuation topics covered in investment banking interviews can be broad and varied. Based on Glassdoor reports from real candidates at Goldman Sachs, J.P. Morgan, and Morgan Stanley, we’ve narrowed down the seven areas you should focus on during your prep.

Below, you’ll also find the top 10 most common interview questions categorized under each topic, along with linked explanations and sample answers:

- What are the three main methods of valuing a company?

- When is a DCF NOT an appropriate valuation method?

DCF

Cost of Capital and WACC

- How do you calculate WACC?

- How do you calculate Cost of Debt and Cost of Equity, and how do they impact a company’s value?

- If the Cost of Equity increases, how does the value of the company change?

Enterprise and Equity Value

Valuation Multiples

LBO Analysis

Advanced and Industry-Specific Valuation

Right, let’s get into each!

2.1 Valuation Methods

The foundation of any banking interview is the "Big Three" valuation methods. Here’s a quick overview:

- Public Comparable Companies ("Public Comps"): A relative valuation method that values a business based on the trading multiples (e.g., EV/EBITDA, P/E) of similar, publicly traded peers.

- Precedent Transactions ("Precedents"): A relative valuation method that looks at the multiples paid for similar companies in past M&A deals.

- Discounted Cash Flow (DCF) Analysis: An intrinsic valuation method that calculates the value of a company by forecasting its future Unlevered Free Cash Flows and discounting them back to the present value using its WACC.

These questions test whether you understand the difference between a) Intrinsic Valuation, which determines a company's worth based on its own future cash flows, and b) Relative Valuation, which determines value based on how the market prices similar companies.

Below are two of the most common questions you might encounter, along with how to approach them.

- What are the three main methods of valuing a company?

- When is a Discounted Cash Flow (DCF) NOT an appropriate valuation method?

a) What are the three main methods of valuing a company? ↑

You should be able to list the three methods, explain the pros and cons of each, and understand why they might produce different results. Note that Analysts typically consolidate these methodologies into a "Football Field" chart to visualize the valuation range.

Sample answer: What are the three main methods of valuing a company?

“There are three primary methods used to value a company: the Discounted Cash Flow (DCF) analysis, Public Comparable Companies, and Precedent Transactions.

First, the DCF provides an intrinsic valuation. You project the company’s Unlevered Free Cash Flows over a five-to-ten-year period and discount them back to the present value using the Weighted Average Cost of Capital (WACC). This gives you a view of what the business is worth based on its specific ability to generate cash in the future, independent of how the market is currently trading.

Second, Public Comparable Companies is a relative valuation method that looks at how similar, publicly traded peers are valued by the market. You analyze trading multiples, such as EV/EBITDA or P/E, and apply those to your target company to estimate its value based on current market sentiment.

Third, Precedent Transactions is also a relative valuation method, but it analyzes the multiples paid for similar companies in past M&A deals. This approach is distinct from the other two because it typically captures a control premium, which is the additional price an acquirer pays to gain full ownership of a target.

Ultimately, analysts use all three methods to triangulate a valuation range. We consolidate these results into a Football Field chart to provide a defensible view of the company’s value in the current market.”

b) When is a Discounted Cash Flow (DCF) NOT an appropriate valuation method? ↑

To answer this question well, you need to show that you understand when a DCF becomes unreliable.

A DCF is highly sensitive to assumptions, especially future cash flow projections. If those are difficult to estimate with confidence, the model’s output becomes less meaningful.

Here’s how to think about when you should (and shouldn’t) use a DCF:

a) Choose a relative valuation method over a DCF when:

- The business has unpredictable cash flows. A DCF is highly dependent on the accuracy of your future cash flow projections. If the business is too volatile, the model becomes unreliable.

- There is not enough financial data available. If you only have access to a company’s revenue, you could perform a relative valuation using a revenue multiple, but you wouldn’t be able to build a full DCF.

- The business is a financial institution. Banks and insurance companies operate differently from a typical cash-flowing business. For example, they profit from the interest spread on debt, which makes traditional Free Cash Flow metrics less relevant.

b) Choose a DCF over a relative valuation when:

- The business is well-established. Companies with highly predictable cash flows are the best candidates for a DCF.

- There are no close comparables. This could be the case for "conglomerate" companies with really varied revenue sources, such as a company that sells both muffins and jet turbines. Without a similar peer group, a relative valuation is difficult to justify.

You can structure your answer as follows:

Sample Answer: When would you use or not use a DCF?

"That’s a good question. I would use a DCF when a company has stable and predictable cash flows, and there is enough information to build a reliable forecast. In those cases, the DCF gives you an intrinsic view of value based on the business’s ability to generate cash over time.

A DCF is also helpful when there are few close comparables or when you want to understand value drivers more clearly than a multiples-based approach allows.

However, I would avoid relying on a DCF when cash flows are volatile or highly uncertain. Early-stage companies, cyclical businesses with large earnings swings, or companies undergoing major transitions are typically better valued using trading comps or precedent transactions. Those methods rely on market data rather than long-term forecasts.

I would also be cautious using a DCF for financial institutions. Their cash generation and capital structures work differently, so book-value-based metrics and comparables tend to provide a more accurate picture.

In practice, I would look at both intrinsic and relative valuation, then lean more heavily on the method that best aligns with the company’s business model and the quality of the available data."

2.2 Discounted Cash Flow (DCF) ↑

According to our analysis of reported questions, Discounted Cash Flow (DCF) is by far the most common technical topic.

DCF is a valuation method that determines the value of a company today based on the present value of its future cash flows. Interviewers use questions, such as “Walk me through a DCF,” to see if you can visualize the entire life cycle of a company’s cash, specifically from revenue to the final Terminal Value.

To calculate it:

DCF = C1 / (1+r)^1 + C2 / (1+r)^2 + … + Cn / (1+r)^n

Note: C = cash flow, r = interest rate (WACC is usually used for this)

Here’s a quick overview of how to answer the “Walk me through a DCF” question:

- Estimate future cash flows (5-10 years into the future)

- Estimate the terminal value of the company

- Convert these numbers to present values using WACC as the interest rate

- Add the numbers together

- The results of this calculation give you the “enterprise value” of the company

Sample answer: Walk me through a DCF

“Sure. A DCF values a company by estimating the cash it will generate in the future and converting those cash flows into today’s value.

I would start by projecting the company’s unlevered free cash flows for roughly 5 to 10 years. These cash flows represent the money the business generates after operating expenses and required reinvestment.

Next, I estimate the terminal value, which captures the value of the business beyond the explicit forecast period. This is usually done using either the Gordon Growth method or an exit multiple.

Once I have both the forecasted cash flows and the terminal value, I discount them back to present value using the weighted average cost of capital, since WACC reflects the risk of the business and the returns required by both debt and equity investors.

Finally, I add the discounted cash flows and the discounted terminal value together to get the enterprise value. From there, I can move to equity value by subtracting net debt and making any other necessary adjustments.

So in summary, a DCF values a company based on its ability to generate cash in the future, adjusted for risk through the discount rate.”

2.3 Cost of Capital and WACC

To value future cash today, you must discount it using a rate that reflects risk. This is where the Weighted Average Cost of Capital (WACC) comes in. These questions test your math skills and your understanding of how a company’s capital structure, meaning its mix of debt and equity, affects its total value.

Here are some common questions you may encounter around this topic:

- How do you calculate WACC?

- How do you calculate Cost of Debt and Cost of Equity, and how do they impact a company’s value?

- If the Cost of Equity increases, how does the value of the company change?

a) How do you calculate Weighted Average Cost of Capital (WACC)? ↑

Based on our analysis, this particular question was only asked in Goldman Sachs interviews, although you will probably still need to understand WACC to answer questions for other firms (including DCF questions).

WACC (Weighted Average Cost of Capital) is the weighted average of a company’s cost of debt and cost of equity.

WACC is also usually the discount rate used in the DCF formula.

In other words, WACC is used to put the “Discounted” in “Discounted Cash Flow,” because it’s the rate used to discount the future cash flows to their present value.

Here’s an overview of how you could answer this question:

- Give the high-level explanation: WACC is the weighted average of a company’s cost of debt and its cost of equity.

- If the interviewer wants to dig deeper, you can discuss the formula in more detail:

- WACC = [Cost of Equity * E/(E + D)] + [Cost of Debt * D/(E+D) * (1 - Tax Rate)]

- Note: E = market value of equity, D = market value of debt

Although this may seem like a straightforward formula question, you’ll often get follow-up questions around how to derive Cost of Equity using the Capital Asset Pricing Model (CAPM) and how to calculate Cost of Debt on an after-tax basis.

Sample Answer: How do you calculate WACC?

"WACC, or the Weighted Average Cost of Capital, measures the return that equity and debt investors expect from the company. It is the company’s financing cost and serves as the discount rate in a DCF since it shows the riskiness of the cash flows.

To calculate it, I start with the Cost of Equity, typically estimated using the Capital Asset Pricing Model (CAPM). That is the Risk-Free Rate plus Beta multiplied by the Equity Risk Premium.

Next, I determine the Cost of Debt, which is the company’s current borrowing rate adjusted for the tax shield because interest expense is tax-deductible.

Once I have both components, I weigh them according to their share of the company’s capital structure. The formula is the Cost of Equity multiplied by Equity over Total Capital, plus the Cost of Debt multiplied by Debt over Total Capital, adjusted for (1 - Tax Rate).

The result is a single rate that shows the return required by all investors, which is why it is used to discount future cash flows in a DCF."

b) How do you calculate Cost of Debt and Cost of Equity, and how do they impact a company’s value? ↑

As mentioned earlier, you can get this as a follow-up to the WACC walkthrough or as a standalone question. A company needs to know its cost of debt and cost of equity for the purpose of making investment decisions and determining its overall valuation.

Cost of Debt is essentially the average interest rate a company pays on its debt. The cost of Equity is the rate of return a company provides to its shareholders to compensate them for the risk of owning the stock.

Here is a brief overview of how to calculate them:

- There are 2 main ways to calculate cost of debt:

- The pre-tax approach: Cost of Debt = Total Annual Interest on Debt / Total Debt

- The after-tax approach: Cost of Debt = Pre-Tax Cost of Debt x (1 - Tax Rate)

- Alternative: Cost of Debt = (Risk Free Rate + Credit Spread) x (1 - Tax Rate)

- The primary method for calculating cost of equity is using CAPM

- CAPM = Capital Asset Pricing Model

- Cost of Equity = (Risk Free Rate + Beta) x (Expected Market Return - Risk Free Rate)

Now, regarding the impact of these two metrics on the valuation of a company:

A company with a high cost of debt is typically riskier and would often have a lower valuation than a comparable company with a low cost of debt.

Similarly, a company with a low cost of equity will likely have a higher valuation than a comparable company with a high cost of equity, because it can get capital for cheaper today to generate more profit in the future.

Sample Answer: How do you calculate the cost of debt and cost of equity? How do they impact a company’s value?

"The Cost of Debt is the effective interest rate a company pays on its borrowings. You calculate it by taking the total annual interest expense divided by total debt, and then adjusting for the tax shield since interest is tax-deductible.

The Cost of Equity is typically estimated using the Capital Asset Pricing Model (CAPM). Under CAPM, the cost of equity equals the Risk-Free Rate plus Beta multiplied by the Equity Risk Premium. This represents the return investors expect for taking on the specific risk of holding that company’s stock.

Together, these components feed into the company’s overall cost of capital, so they directly influence valuation.

A higher cost of debt usually signals more credit risk and increases the discount rate, which lowers the valuation. Conversely, a lower cost of equity generally increases valuation because the company's future cash flows are being discounted at a lower rate, and they can raise capital more cheaply to fund growth.

So, in short, these metrics are critical because they shape the discount rate used to determine the present value of the business."

c. If the Cost of Equity increases, how does the value of the company change? ↑

Interviewers use this to see if you can connect a change in a single input to the final output of a model. Generally, if the Cost of Equity increases, the value of the company decreases.

To explain this further:

- Since WACC is a weighted average of the cost of equity and the cost of debt, an increase in the cost of equity will pull the overall WACC higher, assuming the capital structure stays the same.

- In a DCF, the WACC acts as the discount rate. Mathematically, it sits in the denominator of the present value formula.

- A higher discount rate means that future cash flows are "penalized" more heavily, which reduces the Present Value of those cash flows today.

- From an investor's perspective, a higher Cost of Equity means they perceive the company as riskier. To compensate for that risk, they demand a higher return, which naturally lowers the price they are willing to pay for the business right now.

Sample Answer: If the Cost of Equity increases, what happens to valuation?

"If the Cost of Equity increases, the value of the company decreases.

The reason is that the Cost of Equity is a key component of the WACC. If it goes up, the WACC also increases, assuming the company’s capital structure remains constant.

Since the WACC serves as the discount rate in a DCF, a higher rate reduces the present value of the company’s future cash flows. Essentially, because investors are now demanding a higher return to compensate for the perceived risk, the value of those future dollars is worth less to them today.

So, to summarize, a higher Cost of Equity increases the discount rate, which directly pushes the valuation down."

2.4 Enterprise Value and Equity Value ↑

Bankers distinguish between the value of the entire business operations, known as Enterprise Value, and the portion of that value that belongs only to shareholders, which is Equity Value.

You must be able to move between these two concepts fluently using the "Bridge" formula:

- Enterprise Value = Equity Value + Net Debt (plus other claims like Preferred Stock and Minority Interest)

- Equity Value = Enterprise Value – Net Debt (and other adjustments)

Learn more about the difference between enterprise value and equity value on the Investopedia website.

Now, let’s look at one of the most-asked questions at nearly every major firm, including Goldman Sachs, J.P. Morgan, and Morgan Stanley: “What is the formula for Enterprise Value (EV), and what items flow into it?”

To start, Enterprise Value (EV) is the value of a company’s core business operations attributable to all capital providers. It allows for an apples-to-apples comparison between companies by normalizing for differences in how they are financed.

The Formula

Enterprise Value = Equity Value + Total Debt + Preferred Stock + Non-Controlling Interest - Cash

A few reminders before we get into the sample answer:

- Additions (Debt/Preferred): You add these because they are mandatory claims. An acquirer must pay these off or "assume" them, which increases the total cost of the deal.

- Subtractions (Cash): You subtract cash because it is a non-operating asset. In a transaction, the buyer can use the target’s own cash to "pay itself back," effectively lowering the net price.

Sample answer: What is the formula for Enterprise Value (EV), and what items flow into it?

“There are three primary methods used to value a company: the Discounted Cash Flow (DCF) analysis, Public Comparable Companies, and Precedent Transactions.

First, the DCF provides an intrinsic valuation. You project the company’s Unlevered Free Cash Flows over a five-to-ten-year period and discount them back to the present value using the Weighted Average Cost of Capital (WACC). This gives you a view of what the business is worth based on its specific ability to generate cash in the future, independent of how the market is currently trading.

Second, Public Comparable Companies is a relative valuation method that looks at how similar, publicly traded peers are valued by the market. You analyze trading multiples, such as EV/EBITDA or P/E, and apply those to your target company to estimate its value based on current market sentiment.

Third, Precedent Transactions is also a relative valuation method, but it analyzes the multiples paid for similar companies in past M&A deals. This approach is distinct from the other two because it typically captures a control premium, which is the additional price an acquirer pays to gain full ownership of a target.

Ultimately, analysts use all three methods to triangulate a valuation range. We consolidate these results into a Football Field chart to provide a defensible view of the company’s value in the current market.”

2.5 Valuation Multiples ↑

Multiples are a shorthand way to value a company by comparing it to its peers. Interviewers want to see if you know which "yardstick" to use for different industries.

These questions test whether you understand capital structure neutrality and can correctly match the numerator and denominator of a multiple.

In banking, the golden rule for multiples is that the numerator (the value) must match the denominator (the earnings flow).

- EV/EBITDA is an Enterprise Value multiple. Because EBITDA is calculated before interest is paid, it represents the earnings available to all capital providers, both Debt and Equity.

- P/E is an Equity Value multiple. Because Net Income (the "Earnings") is calculated after interest is paid, it represents the profit available only to shareholders.

Right, let’s look at this common multiple question: “When would you use a Price-to-Earnings (P/E) ratio versus an EV/EBITDA multiple?”

Here is a brief overview of when to use each:

- Use EV/EBITDA when you want to compare companies with different capital structures. Because it is "above the interest line," it isn't affected by how much debt a company has. It is the standard for most capital-intensive industries, such as Manufacturing or Energy.

- Use P/E for established, stable companies where interest and taxes are fairly consistent. It is the most common metric for everyday investors, but it can be distorted by high debt loads or significant non-cash expenses like Depreciation.

Sample Answer: When would you use a P/E ratio versus an EV/EBITDA multiple?

"It depends on whether you want to value the entire business or just the portion attributable to shareholders.

I would use EV/EBITDA when I need a capital structure-neutral metric. Because EBITDA is an unlevered flow, meaning it is calculated before interest and taxes, it allows for a direct comparison between companies regardless of how they are financed. This is why it is the preferred multiple for most M&A transactions and capital-intensive industries.

On the other hand, I would use P/E when I am focused specifically on the value available to equity holders. Since Net Income is a levered flow that accounts for interest and taxes, P/E tells you what the market is willing to pay for a dollar of bottom-line profit. It is most effective for comparing mature companies with similar capital structures, such as those in the banking or insurance sectors.

So, to summarize, I would use EV/EBITDA when comparing the operational value of different businesses, and P/E when comparing the specific returns available to their shareholders.”

2.6 Leveraged Buyout (LBO) Analysis ↑

As a refresher: an LBO is an acquisition of a company made using a significant amount of debt. The target company’s cash flows are then used to service and pay down that debt over time, "shifting" the value of the company from the lenders to the equity owners.

The success of an LBO is determined by three primary financial levers:

- The Purchase Price: The entry multiple (valuation) paid for the business.

- The Leverage: The amount of debt used and the interest rate (cost of debt).

- The Exit Price: The valuation multiple at which the firm ultimately sells the business.

LBO analysis questions test your understanding of debt, returns, and exit strategies.

Below is a common question you can get around LBO analysis.

Sample Answer: What is an LBO, and what are its value drivers?

"An LBO, or leveraged buyout, is when a financial sponsor acquires a company using a significant amount of debt to finance the purchase. The idea is that using leverage amplifies equity returns as the company uses its cash flow to pay down that debt over the holding period.

There are three main drivers that determine whether an LBO is successful:

First is the purchase price. The lower the entry valuation, the greater the potential for equity upside when the firm eventually exits the investment.

Second is the amount and cost of debt. Using a higher percentage of debt can boost returns, but only if the company’s cash flows can comfortably cover the interest and principal payments.

Third is the exit price. This is the valuation at which the firm ultimately sells the business. Exiting at a higher multiple than the entry, or after significantly improving profitability, increases the total return.

In addition to these financial drivers, you should also take note of operational improvements. Firms look for opportunities to increase cash flow by cutting costs, improving working capital, or growing revenue. These changes allow the company to pay down debt more quickly and support a much higher equity value at exit."

We recommend watching the video below to develop a deeper understanding of LBOs and how they work:

2.7 Advanced and Industry-Specific Valuation ↑

At top-tier firms, you will be asked to apply valuation theory to tricky, real-world scenarios. This tests your intuition, as it determines if you can value a company that doesn't fit the standard textbook mold.

Expect questions, such as “How would you value X company?”, designed to test whether you can match a business model to the correct valuation method.

As an example, you might be asked: "How would you value Morgan Stanley?"

To approach this question:

- Identify the Business Model: Morgan Stanley is a diversified financial institution. Unlike a manufacturing firm, its "inventory" is money, and its "cost of goods sold" is interest.

- Select the Primary Method: Financial institutions are almost always valued using Relative Valuation, specifically the Comparable Companies method.

- Choose the Right Multiple: I would use the Price-to-Book Value (P/BV) or Price-to-Tangible Book Value (P/TBV) multiple.

- The Logic: Banks are highly regulated and required to "mark-to-market" their assets and liabilities. This means their Balance Sheet is a much more accurate reflection of market value than it would be for a software or retail company.

Sample Answer: How would you value Morgan Stanley?

"First, I would start by understanding the type of business we’re valuing, because the approach can change depending on the industry. For example, if the company is a bank like Morgan Stanley, traditional metrics such as EBITDA or free cash flow are less meaningful since banks generate value through interest income and their balance sheets are marked to market.

In that case, I would rely primarily on a Comparable Companies analysis using industry-specific multiples. For banks, the most common metric is Price-to-Book Value, since book value closely reflects the fair value of their assets and liabilities.

I would identify a set of comparable banks with similar business models, geographies, and risk profiles, analyze their trading multiples, and apply the appropriate range to the target company. I would also look at Comparable Transactions to see how similar institutions were valued in recent M&A deals, since those multiples often include control premiums.

If additional information were available, I might also consider a dividend discount model or residual income model, which can be more appropriate for financial institutions than a standard DCF.

After reviewing these methods, I would triangulate a valuation range and explain which approach I would weight most heavily and why."

3. More examples of IB valuation interview questions (by company) ↑

The questions in Section 2 cover the most commonly asked valuation topics, but each major investment bank tends to have its own specific focus.

Our analysis of recent Glassdoor reports shows that Goldman Sachs tends to focus on intrinsic valuation and the logic behind DCFs, J.P. Morgan often emphasizes relative valuation and market-based multiples, and Morgan Stanley usually asks candidates to connect valuation concepts to capital structure and shifts in Enterprise Value.

Below, you’ll find a list of company-specific valuation examples you can practice with from Goldman Sachs, J.P. Morgan, and Morgan Stanley.

Example of Goldman Sachs IB valuation questions

- What are the main methods of valuing a company?

- Walk me through a Discounted Cash Flow (DCF).

- Explain Weighted Average Cost of Capital (WACC) and how to calculate it.

- What happens to the Weighted Average Cost of Capital (WACC) of a company in debt?

- How would you value X company?

- How do you value a company with no revenue or profit?

- How do you calculate the market capitalization of a company?

- If cost of equity increases, how does the value of the company change?

- If you could choose a Price-to-Earnings (P/E) ratio of 8 or 10, which would you pick?

Check out our Goldman Sachs interview guide for more company-specific insights and information.

Example of J.P. Morgan IB valuation questions

- Walk me through a Discounted Cash Flow (DCF).

- What are the ways to work out a company's value?

- Talk to me about some leverage ratios you may use to value the risk on the company's balance sheet.

- Value Airbnb using Discounted Cash Flow (DCF), Leveraged Buyout (LBO), and Comparable Company Analysis (Comps).

- When would you not use a Discounted Cash Flow (DCF) to evaluate a company?

- How would a Discounted Cash Flow (DCF) change for a company in the biotechnology space?

- How would you value a company, aside from the traditional valuation method?

- How would you personally look to ascribe value to a company?

- How would you do the valuation of a car washing business?

Check out our J.P. Morgan interview guide for more company-specific insights and information.

Example of Morgan Stanley IB valuation questions

- Walk me through a Discounted Cash Flow (DCF).

- What are the ways to value a company?

- What is Enterprise Value (EV)?

- What items flow into the Enterprise Value (EV) formula?

- How would you value a private company?

- Give me a scenario for when a Discounted Cash Flow (DCF) is more valuable than the multiples method.

- What is a Leveraged Buyout (LBO) and how does it work? What are its primary value drivers?

Check out our Morgan Stanley interview guide for more company-specific insights and information.

4. Tips to ace your IB valuation interviews ↑

As you can see from the complex questions above, there is a lot of ground to cover when it comes to investment banking interview preparation. So it’s best to take a systematic approach to make the most of your practice time.

Below are 8 useful tips to help you prepare for your IB valuation interviews.

4.1 Familiarize yourself with deals related to the company

Real-world deals come up frequently in investment banking interviews, as interviewers want to see if candidates really understand the industry and the important factors to consider when valuing a deal.

You should prepare to discuss a couple of recent investment banking transactions in depth, particularly in relation to their valuation drivers and purchase multiples.

Be ready to give your opinion on why the deal was a good (or bad) move, and memorize key figures like the Transaction Value and Enterprise Value to EBITDA multiples to back up your analysis.

If you’re applying for a particular group within your target firm, make sure you prepare to discuss deals that are relevant to that group’s specific sector.

4.2 Be prepared to talk about the economy and financial markets

Understanding the broader economy is essential for investment bankers because market conditions directly affect a company’s financial performance and, by extension, its total valuation.

You should be ready to explain how changes in global and regional markets might affect a company’s cost of capital, discount rates, and future growth projections.

Be ready to give your views on:

- Macroeconomic trends (e.g., how inflation impacts operating margins)

- Central bank policy (e.g., how rate hikes increase the Weighted Average Cost of Capital)

- Market movements (e.g., how sector performance influences trading multiples)

- Recent transactions (e.g., how current market shifts are influencing valuations or deal structures)

To stay current, you can review market updates and analysis from reliable sources such as The Financial Times, The Wall Street Journal, Bloomberg, Reuters, and CNBC.

4.3 Refresh your memory with a cheat sheet

When it comes to technical questions in particular, a cheat sheet is useful for a quick refresher on accounting concepts.

Of course, bringing one to in-person interviews is not the best idea, and even using one for video interviews would not look great. However, it can be useful to reference during initial phone screens (assuming you won’t be on video), while answering practice questions, and as a refresher immediately before an interview begins.

That said, it's important not to become too reliant on it. Hashim (ex-Lazard Analyst, ex-JP Morgan) says that memorizing terms is a common mistake he observes in candidates. You should focus on understanding the connections between concepts so that if one factor changes, you can still confidently adapt and reframe your answer.

You can check out our investment banking interview cheat sheet, with information around DCF, valuation, the financial statements, and a few additional formulas.

4.4 Be comfortable performing quick mental math

Calculators are not usually allowed in investment banking interviews. You won’t need to perform complex modeling, but you will need to handle basic mental arithmetic and valuation ratio logic (e.g., quickly estimating an Enterprise Value based on a multiple).

If you’re out of practice, regularly exercise your mental math muscle to become as fast and accurate as possible. Khan Academy has several helpful resources for refreshing your arithmetic skills. Here are a few we recommend:

Once you're feeling comfortable with the basics, you'll need to regularly exercise your mental math muscle to become as fast and accurate as possible.

You might want to use some of the following resources. We haven't tested all of them, but some of the candidates we work with have used them in the past and found them helpful.

- Preplounge's math tool. This web tool is very helpful to practice additions, subtractions, multiplications, divisions, and percentages. You can both sharpen your precise and estimation math with it.

- Mental math cards challenge app (iOS). This mobile app lets you work on your mental math easily on your phone. Don't let the old-school graphics deter you from using it. The app itself is actually very good.

- Mental math games (Android). If you're an Android user, this one is a good substitute for the mental math cards challenge one on iOS.

4.5 Practice with real financial statements

A high percentage of your valuation interview questions will require you to pull data from financial statements. It only makes sense to get hands-on experience by reviewing real company filings.

Real filings are far more complex than the simplified examples found in prep guides. By studying the financials of a company like Microsoft, you can learn how to identify the "clean" numbers needed for a valuation, such as Net Debt or Unlevered Free Cash Flow. This practice helps you prepare for the sophisticated level of analysis required at firms like Goldman Sachs.

4.6 Catch the hints

In valuation, there is often a range of "correct" answers rather than a single number. Most interviewers have good intentions and may give you subtle hints about where to take your answer.

If an interviewer questions one of your assumptions, such as your Exit Multiple or Discount Rate, follow their lead. They are likely trying to steer you toward a more standard industry range. Candidates sometimes get so stressed that they miss these cues, but picking up on a hint shows that you are coachable and have strong financial intuition

4.7 Perform a sanity check

When valuing an asset, it is easy to get caught up in the formulas. Interviewers will often test whether you can step back and ask if a valuation actually makes sense.

For instance, if your DCF shows a target is worth double its current market price, you need to be able to explain that gap or identify which of your assumptions is too aggressive. Showing that you can catch your own outliers proves you have the judgment required on the job.

4.8 Understand the Valuation Hierarchy

You will often be asked which valuation method produces the highest or lowest value. While it depends on the scenario, there is a standard order: Precedent Transactions typically yield the highest valuation because they include a "control premium" paid to own the entire asset.

Public Comps are usually lower because they reflect minority stakes without that extra cost. Explaining these relationships shows you understand the strategic context of a transaction, not just the math behind the numbers.

5. How to prepare for IB valuation interviews ↑

Valuation interviews are technically rigorous. You’ll need to bridge concepts, evaluate trade-offs, and defend your logic clearly. However, they’re manageable if you prepare properly.

Use every resource available to you. This could include your network, upperclassmen, alumni, school clubs, mentors, or peers.

For example, you can speak with someone who has interviewed for a valuation role at your target firm, run mock technicals and case-style questions with classmates, or ask a mentor for feedback on your valuation approach.

In addition to that, we’d also like to share some resources to help you prepare.

5.1 Research the company you’re applying to

In many cases, investment banking valuation interview questions will be tied to the company’s actual deals and client base. If you’re applying to a specific team, study their recent transactions, industry coverage, and priorities.

Take the time to understand which types of clients or projects you’d most likely be working on based on the job description, and research them thoroughly. Look up relevant deal announcements, investor presentations, and press releases so you can speak confidently about the company’s recent activities and how you would contribute to similar transactions.

If you want to learn more about your target firm, check out the resources below. We’ve included useful links for the top 8 firms commonly regarded as “bulge bracket” banks, known for their large-scale deals and rigorous hiring processes:

Goldman Sachs

- Goldman Sachs’ purpose and values (By Goldman Sachs)

- Goldman Sachs Briefings newsletter (By Goldman Sachs)

- Goldman Sachs strategy teardown (by CB Insights)

J.P. Morgan

- Who we are (By JP Morgan)

- JP Morgan weekly brief (By JP Morgan)

- JP Morgan strategy teardown (by CB Insights)

Morgan Stanley

- A culture-driven strategy (by Morgan Stanley)

- Insights (by Morgan Stanley)

- Comparison Morgan Stanley vs Goldman Sachs (by Investopedia)

Bank of America

- Bank of America core values (by Bank of America)

- BofA Insights (by Bank of America)

- BoFa strategy teardown (by Rancord Society)

Citigroup

- About Citi

- Insights (by Citi)

- Citi’s plan to transform its wealth business (by Euromoney)

Barclays Capital

- About Barclays

- Barclays’ three-year plan (by Barclays)

- Barclays’ official interview prep guide (by Barclays)

UBS Investment Bank

- About UBS

- UBS sustainability and impact strategy (by UBS)

- UBS checklist for interview prep (by UBS)

Deutsche Bank

- About Deutsche Bank

- Deutsche Bank strategy (by Deutsche Bank)

- Deutsche Bank interview prep guide (by Deutsche Bank)

5.2 Practice by yourself

Acing behavioral questions is harder than it looks. You’ll stand out if you put in the required work to craft concise and direct answers.

We recommend starting with our guides below to prepare for your valuation interviews. You’ll also find a few additional articles that can help you understand the full IB interview process:

General

- Investment banking interview prep guide

- Investment banking interview questions guide

- 15 investment banking interview tips

- Investment banking interview cheat sheet

- How to answer “Why X company” question

- Investment banking technical questions guide

- Investment banking behavioral & fit questions guide

- Investment banking interview accounting questions guide

- Investment banking brainteasers guide

- Investment banking HireVue interview guide

- Investment banking Superday interview guide

- How to network your way into investment banking (by ex-Merrill Lynch director Mike)

- How to make your LinkedIn profile more visible to IB recruiters (by ex-Merrill Lynch director Mike)

- Investment Banking Fit Questions Masterclass (by ex-Blackstone MD Kent)

Goldman Sachs

- Goldman Sachs interview prep guide

- Goldman Sachs behavioral interview guide

- Goldman Sachs HireVue interview guide

J.P. Morgan

- JP Morgan interview prep guide

- JP Morgan behavioral interview guide

- JP Morgan HireVue interview guide

Morgan Stanley

- Morgan Stanley interview prep guide

- Morgan Stanley behavioral interview prep guide

- Morgan Stanley HireVue interview guide

5.3 Practice with peers

If you have friends or peers who can do mock interviews with you, that's an option worth trying. It’s free, but be warned, you may come up against the following problems:

- It’s hard to know if the feedback you get is accurate

- They’re unlikely to have insider knowledge of interviews at your target company

- On peer platforms, people often waste your time by not showing up

For those reasons, many candidates skip peer mock interviews and go straight to mock interviews with an expert.

5.4 Practice with ex-investment banking interviewers

In our experience, practicing real interviews with experts who can give you company-specific feedback makes a huge difference.

If you know someone who runs interviews at an investment bank, then that’s amazing! They'll be a great person to practice interviews with.

But most of us don’t, and it can be REALLY tough to make a new connection with an investment banker. And even if you do have a good connection already, it might also be difficult to practice multiple hours with that person unless you know them extremely well.

That’s where mock interviews come in.

Find an investment banking interview coach so you can:

- Test yourself under real interview conditions

- Get accurate feedback from a real expert

- Build your confidence

- Get company-specific insights

- Save time by focusing your preparation

Click here to book investment banking mock interviews with experienced finance interviewers.